May 8, 2026

U.S. Cannabis: One Sector, Forty-Five Markets

Understanding Fragmentation, Diversification, and Structural Premia in U.S. Cannabis Credit

Q2 2026

The views expressed are general market observations, provided for informational purposes only, and do not constitute investment advice.

Introduction

Diversification is a foundational principle of credit allocation—yet in private markets, it is often more illusory than real. Portfolios presented as diversified—across industries, sponsors, and borrowers—are frequently exposed to a common set of underlying risk factors: leverage cycles, private equity exit dynamics, and broadly syndicated credit conditions.

Against that backdrop, a cannabis-only credit strategy is often perceived as a concentrated sector bet. In practice, however, the U.S. cannabis market behaves less like a single integrated industry and more as a series of distinct credit ecosystems, shaped by federal illegality and state-level regulation.

What appears to be concentration is, in reality, a form of jurisdictional diversification. For a focused senior secured lender, this fragmentation can create an embedded advantage: differentiated exposure across state markets, while regulatory and operational complexity tends to reinforce incumbent positioning. Over time, this dynamic tends to preserve pricing discipline and create access to opportunities less efficiently intermediated elsewhere.

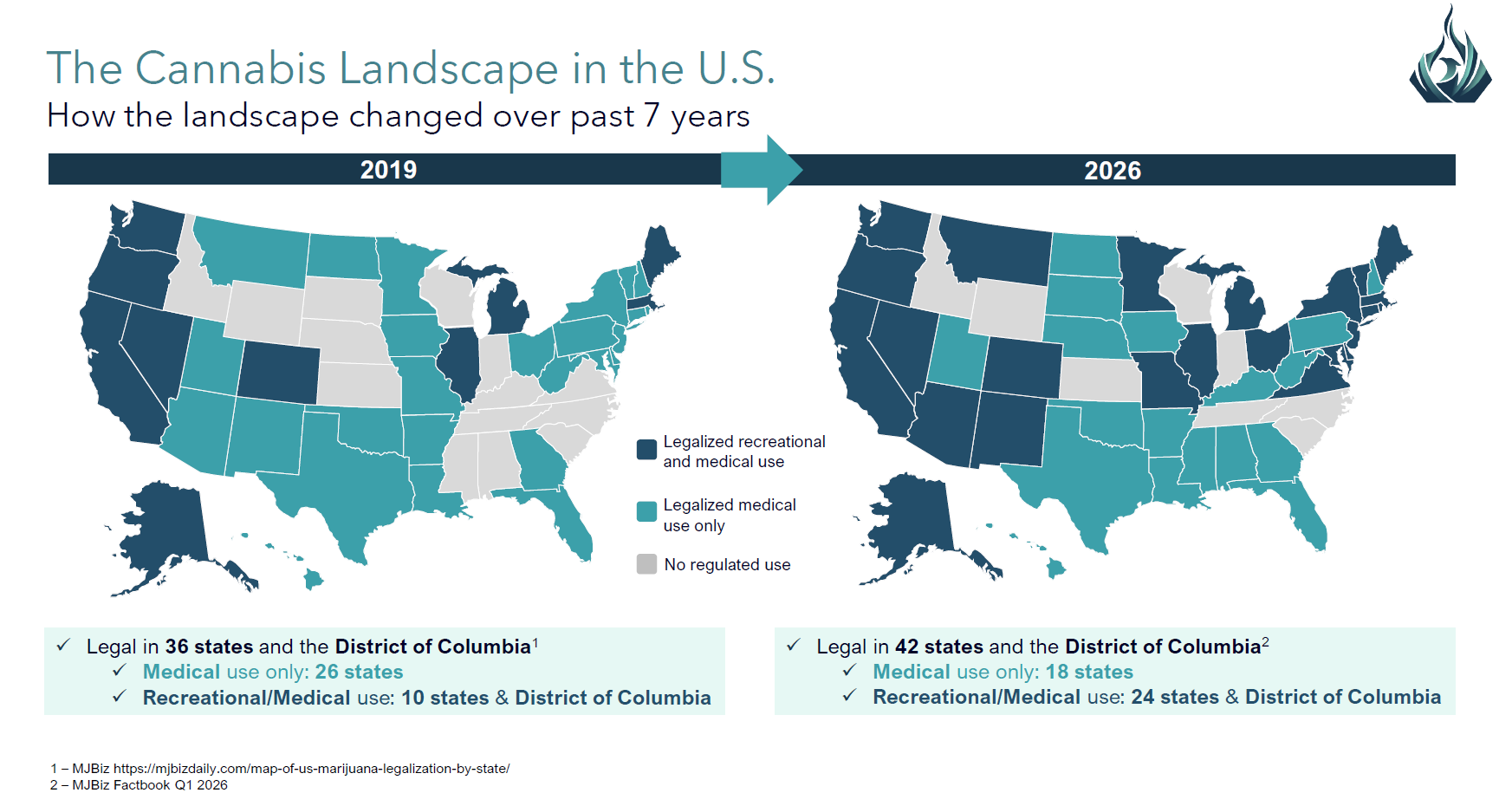

One label, many markets

Cannabis remains illegal at the federal level even as a growing majority of states have legalized medical and, increasingly, adult-use cannabis.

Because interstate commerce is effectively blocked for plant-touching businesses, each state has constructed its own framework for licensing, taxation, ownership rules, and local control.1 The result is a patchwork of more than forty distinct legal markets with limited cross-border spillover.

From a credit perspective, a loan to an operator in a limited-license East Coast state backed by scarce dispensary licenses behaves very differently from a loan to an operator in an open-license Western cultivation market, even though both are categorized as cannabis.2

Diversification through low correlation3

Fundamentals are driven locally. Pricing and margins depend largely on state-specific capacity, license density, and consumer mix.

Regulatory risk and competitive intensity are state- and municipality-dependent rather than purely federal and reflect license caps, zoning, and local enforcement practices.

A portfolio that deliberately caps per-state and per-borrower exposure and blends adult-use and medical-only markets can achieve low correlation among underlying credits inside a single industry label.

The core of diversification lies in the nature of the risk itself: it is jurisdictional and idiosyncratic, not systemic. Cannabis does not exhibit a single, unified beta.

Turning fragmentation into a competitive moat

Regulatory and relationship capital

State-by-state complexity creates a high bar for new lenders. Early entrants that have already executed and monitored dozens of loans across multiple states have accrued detailed knowledge of regulatory regimes and change-of-control mechanics, deep relationships with leading operators and local stakeholders, and process know-how around structuring collateral and remedies within each state’s rules.

This combination of regulatory and relationship capital can enhance underwriting outcomes and, by its nature, is slow to replicate.

Underwriting and selection edge

First-mover platforms in cannabis private credit have built proprietary datasets of operator performance, unit economics, and regulatory behavior across states and sub-segments such as cultivation, processing, and retail. That information advantage supports better state selection, tighter structuring calibrated to local risk, and more rational pricing of uncertainty.

For allocators, the key question is not whether cannabis is one sector. The better question is which lender has the underwriting experience and state-specific insight to convert fragmentation into a structural advantage.

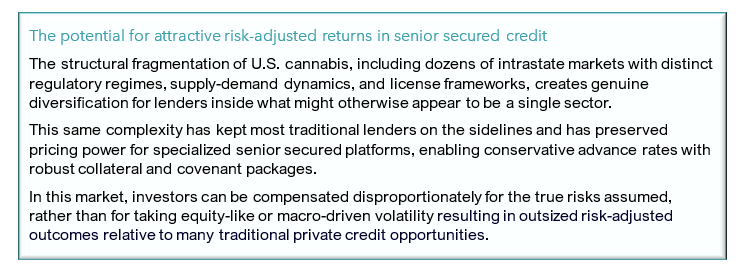

Why the market overpays senior secured lenders

Capital scarcity and favorable risk-adjusted economics

Federal illegality and reputational concerns constrain traditional banks and many mainstream credit funds from lending to state-legal operators. Ongoing volatility and sustained periods of dislocation in public cannabis equity markets have limited access to cost-effective capital, creating a funding gap that specialized private credit platforms are well positioned to address.

In this gap, leading senior secured lenders have disclosed portfolios characterized by predominantly first-lien loans, conservative loan-to-value ratios frequently in the 40 to 60 percent range, sometimes supplemented by fees and selective equity participation.

Senior secured, asset-backed lending in cannabis is offering the potential for equity-like returns because of regulatory and structural complexity rather than fragile fundamentals.

Structural downside protection

Collateral packages typically include real estate, fixtures and equipment, and equity pledges, structured to comply with state licensing rules.

Limited license counts and local barriers to entry can support recoveries in stress by preserving the economic value of incumbent footprints, since new competitors cannot easily rush in and replicate those licenses. Combined with conservative advance rates and active covenant monitoring, this has the potential to produce asymmetric outcomes: current income, diversified by state and borrower, with the expectation of manageable loss severity when issues arise.

What does this mean for credit allocators?

For sophisticated and credit-focused allocators, the key reframing is straightforward. The cannabis label obscures the reality that exposures are diversified across dozens of intrastate markets with distinct legal and economic drivers.

Fragmentation and regulatory complexity have created durable competitive moats for first-mover senior secured platforms with established track records and regulatory domain expertise.

The market compensates these lenders with the potential for attractive, complexity-driven returns at the senior secured level.

In other words, great diversification is built into the structure of the U.S. cannabis industry, and specialized senior secured lenders are uniquely positioned to potentially convert that structural feature into both downside protection and attractive risk-adjusted yield.

Conclusion: The Credit Manager’s Opportunity

For the sophisticated allocator, the U.S. cannabis market is not a commodity exposure, but a multi-jurisdictional credit strategy.

Federal prohibition has produced a fragmented system of state-level markets, each operating with independent supply-demand dynamics, regulatory frameworks, and capital constraints. What appears to be a single sector is, in practice, a collection of discrete lending environments.

For senior secured lenders, that structure is the opportunity. It supports persistent pricing power, strong collateral protections, and genuine jurisdictional diversification within a single thematic allocation.

Realizing that opportunity depends on consistent access to high-quality borrowers, disciplined underwriting across market cycles, and the ability to deploy institutional capital across jurisdictions—advantages typically concentrated among a small number of established platforms.

What appears to be concentration in a single industry is, in reality, diversification across dozens of decoupled markets—a profile difficult to replicate in traditional credit.

Sources

1. The Case for Interstate Marijuana Commerce Right Now, Reason Foundation, 2024, https://reason.org/wp-content/uploads/case-for-interstate-marijuana-commerce-right-now.pdf

2. Competition and Market Structure of the U.S. Cannabis Industry, Secretariat International, April 2, 2026, https://secretariat-intl.com/insights/competition-and-market-structure-of-the-u-s-cannabis-industry/

3. Where is Cannabis Legal in North America in 2026?, Cova Software, April 5, 2026, https://www.covasoftware.com/blog/where-is-cannabis-legal-in-north-america-in-2026

Disclosures and Important Information