July 10, 2026

Emerging Markets: Critical Minerals Need Critical Capital

By Jim Garvey, CFA ©, Peter Marber, PhD, FRSA, FRAS

For all the talk of clouds, chips and artificial intelligence, the modern economy remains stubbornly geological. Batteries need lithium, nickel, cobalt and graphite; chips and sensors need gallium, germanium, indium, tantalum and high-purity silicon; motors, turbines, smartphones and missiles need rare-earth magnets. Copper, the workaday metal of wiring, may be the most strategic of all.

Modern growth, AI infrastructure and national security are all bound together. An overreliance on one country’s market share in key minerals can turn commercial dependence into a national-security vulnerability. The vulnerability is sharper because refining and processing are often more concentrated than mining. The International Energy Agency (IEA) reports that, for copper, lithium, nickel, cobalt, graphite and rare earths, the average market share of the top three refining countries rose to 86 percent in 2024, with China the dominant supplier for most of those chains (Berg et al., 2024; IEA, 2025).

Today’s demand is already outrunning the old supply-chain model. The IEA reported that lithium demand has been rising by 30 percent, while demand for nickel, cobalt, graphite, and rare earths is also accelerating and could rise by nearly 500 percent by 2050, requiring more than three billion tons of minerals and metals for clean-energy deployment (IEA, 2021, 2025; World Bank, 2020).

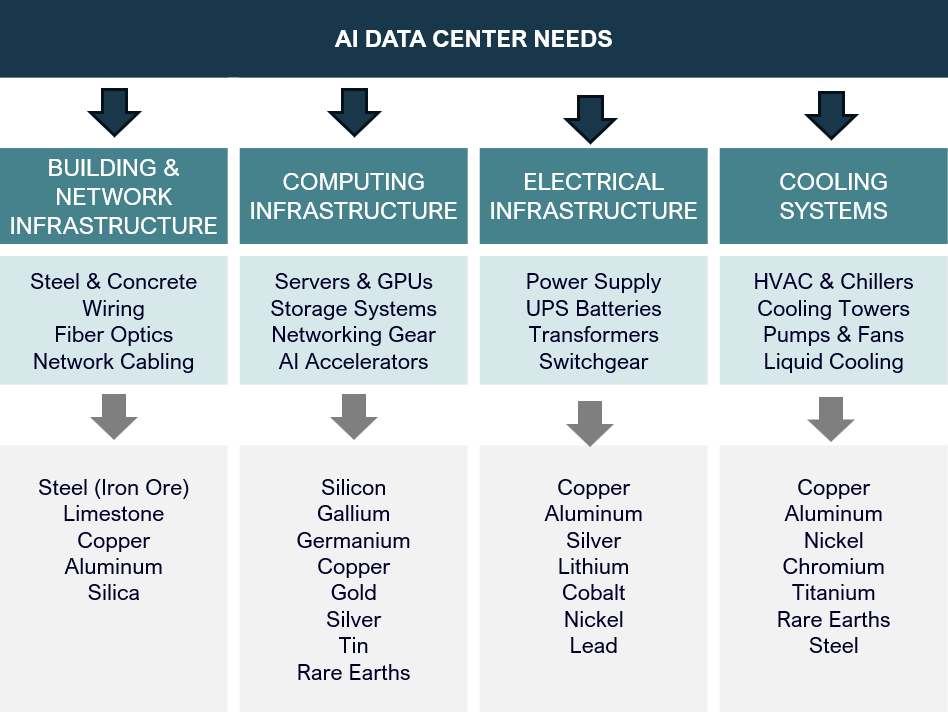

Exhibit 1: Most Important Critical Minerals for AI

- Copper: Power delivery, wiring, cooling systems

- Silicon: Semiconductors and AI chips

- Rare Earths: Motors, fans, drivers, magnets

- Gallium: Advanced power semiconductors

- Germanium: Fiberoptics and communications

- Lithium: Battery backup systems

- Nickel: Batteries and cooling equipment

- Silver: High-conductivity electrical contacts

- Gold: Chip packaging and reliability

- Aluminum: Power distribution and heat management

Emerging Markets to the Rescue?

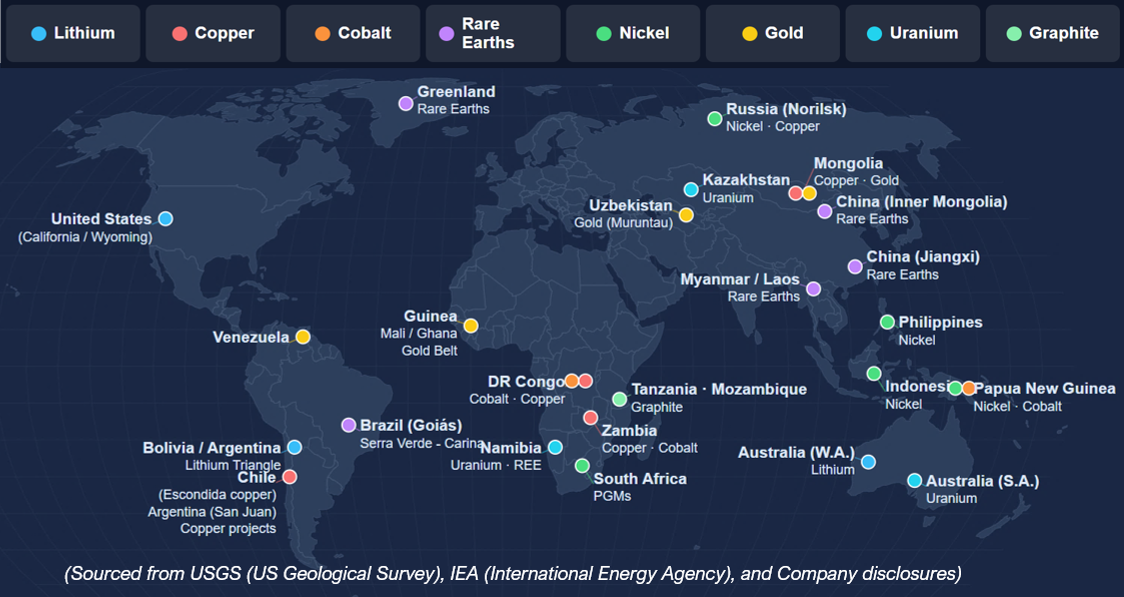

These desirable geological resources, however, are not only in the countries pushing the technological envelope; they’re in the Emerging Markets of Asia, Africa, Latin America, the Middle East and former Soviet republics.

The Democratic Republic of the Congo and Zambia sit on the copper-cobalt belt. Chile and Peru straddle large copper deposits; Argentina, Chile and Bolivia form the lithium triangle. Brazil has become one of the most watched rare-earth jurisdictions outside Asia. Indonesia has used nickel to wedge itself into the battery supply chain. Mongolia’s Oyu Tolgoi and Pakistan’s Reko Diq show the scale of Asian copper development. Namibia, Angola and other African jurisdictions are being drawn into rare-earth, logistics and processing plans. Interestingly, countries in the Gulf – especially Saudi Arabia – are increasingly acting as a capital and offtake platform for global mineral assets rather than merely a hydrocarbon exporter (Asian Development Bank, 2025; Barrick Mining Corporation, n.d.; Global Minerals Report, 2026; Public Investment Fund, n.d.; Rio Tinto, n.d.; Vale, 2024).

Massive projects are being announced daily. In Africa, the Lobito Corridor is designed to connect Angola’s Atlantic port to mineral-rich areas of the DRC and Zambia; DFC has supported rare-earth processing in Angola and a Western Hemisphere rare-earth supply chain through Aclara’s Carina project in Brazil; and the European Union has a strategic raw-materials partnership with Namibia. In Latin America, the EU’s Global Gateway program has a lithium and copper value-chain initiative in Argentina and Chile. Rio Tinto’s Rincón lithium expansion and McEwen Copper’s Los Azules project show how Argentina is trying to translate geology into bankable development under its large-investment regime. In Asia, Oyu Tolgoi is ramping up one of the world’s major copper mines in Mongolia, while Reko Diq in Pakistan is being financed with multilateral support and aims at first production later this decade. In the Middle East, Saudi Arabia’s Manara Minerals has bought into Vale Base Metals and is explicitly targeting future-facing minerals and offtake security.

(Asian Development Bank, 2025; European Commission, 2022, n.d.; McEwen Mining, 2025; Rio Tinto, 2024; U.S. International Development Finance Corporation [DFC], n.d., 2024, 2025a, 2026; Vale, 2024).

Exhibit 2: Global Critical Minerals: Deposit Locations

Private Credit to the Rescue?

While we can easily draw the geological map, the landscape for capital is less defined. Many lessons have been learned from similar past commodity super-cycles in the 1960s and 1970s when multinationals often negotiated shady deals with corrupt regimes, leaving developing countries with depleted resources while sitting on mountains of debt owed largely to foreign banks.

Host countries and industrial players today both understand that a modern mine is more than a shovel and a pit. It is a geological model, an environmental and labor plan, a power and water strategy, rail or port access, offtake contracts, processing capacity, political-risk management, and a balance sheet that needs to survive years before cash flow.

The IEA’s review of major mines that came online between 2010 and 2019 found an average of more than sixteen years from discovery to first production. Unfortunately, these timelines don’t align with the local emerging financial system that has relatively small balance sheets and short-dated funding. Multibillion-dollar mines and rail-and-port corridor projects do not fit easily onto the books of most local lenders (IEA, 2021; World Bank, 2024).

This is the core bottleneck in critical minerals, the classic mismatch: Emerging Market banks can help with funds for deposits, payroll, working capital, and local-currency relationships, but their liabilities are often short-dated and domestic, while mining construction costs are long-dated, dollarized and exposed to commodity, permitting and political cycles. Global capital is needed to fill the gaps.

This is why private credit should be central to the next stage of the Emerging Market critical mineral story. Properly underwritten private credit can do what commercial banks and plain-vanilla equity often cannot.

Private credit can provide construction debt, mezzanine capital, bridge-to-feasibility loans, secured pre-export finance, royalty-and-streaming hybrids, receivables facilities, and inventory-backed structures tied to real offtake. It can price illiquidity, take security over project assets and contracts, and match repayment to production curves. Most importantly, it can stand between strategic demand from buyers and the local financing gap at the asset level.

The best private credit funds will behave less like yield tourists and more like project-finance operating partners: they must understand metallurgy, permitting, community risk, shipping constraints and buyer concentration, not merely credit spreads.

The trend is beginning to emerge. The International Finance Corporation (IFC) has been instrumental in the metals and mining value chain with equity, quasi-equity, project-level debt and third-party mobilization, and has begun to mobilize more funding. It recently announced a dedicated US$1 billion critical minerals and metals fund for Emerging Markets, including an IFC anchor commitment and exposure across equity, credit, and royalties. The U.S. International Development Finance Corporation (DFC) has joined a US$1.8 billion Critical Mineral Consortium designed to address financing gaps in strategic mineral projects in DFC-eligible markets. The Forum on Resource Geostrategic Engagement (FORGE) was created to coordinate DFIs and export-credit agencies around responsible critical-minerals projects. EXIM’s Project Vault adds a demand-side tool: a US$10 billion loan, paired with private capital, for a strategic critical-minerals reserve that gives manufacturers a supply backstop.

(Appian Capital Advisory, 2025; DFC, 2025b; Export-Import Bank of the United States, 2026; International Finance Corporation [IFC], 2025; U.S. Department of State, 2024)

Structure Matters

For investors, this critical mineral opportunity is not generic “mining beta.” It is a more complicated credit-selection problem. Not all projects will work, and investors will need to align themselves with managers experienced with Emerging Markets risks – particularly country, partner and project selection. They need to understand a range of needed due diligence including independent reserve reports, audited capex requirements and completion-support packages, along with project-specific anti-corruption covenants.

The best financial investments in Emerging Markets may often be blended with government and multilateral links without becoming bureaucratic. For example, Development Financial Institutions (DFIs) and Export Credit Agencies (ECAs) may be useful for first-loss positions, political-risk insurance, fund feasibility work or anchor senior tranches. Private credit can then provide scale, speed and structuring discipline. Local banks can still participate, but mainly where they add local-currency facilities, payroll, vendor finance and regulatory knowledge.

Most importantly, long-term commodity projects and financial structures in the 2020s and beyond require more sustainable planning and transparency than the one-sided extraction deals of the past. This is non-negotiable. These commodity supply links are now seen as vital public policy in the US and

elsewhere; they are foundational elements for modern economies and defense.

While today’s mineral critical capital might still come from the West, most likely it will be part of larger infrastructure projects that finance power, water, rail, processing, training, reclamation and local suppliers alongside the mines.

Moreover, instead of the finance being the sole domain of large American and European commercial banks as it was in the 1960s and 1970s, today’s deals will bring a much broader mix of financial players taking defined risk positions in complex capital structures.

Looking Ahead

The conclusion is clear: critical minerals need critical capital. The world has enough geological promise to reduce supply-chain concentration, but not enough bankable financing structures to move quickly.

The countries that win the next phase of industrial competition will be those that connect strategic buyers, DFIs, export-credit agencies, local institutions and specialist private credit into repeatable project-finance templates. For Emerging Markets, that means turning their resource endowments into infrastructure, jobs and processing capacity. For private credit funds, it is a chance to finance hard assets that sit at the center of today’s technology, energy and security. The right loan to the right mine, railway or refinery is no longer just a yield instrument. It is an investable piece of industrial and security policy.